Aug 22, 2024

Claudine Hood has seen a lot of patients dealing with complex medical bills. With more than 20 years as a medical billing professional, she knows that people often find it difficult to understand their medical bills.

Aug 22, 2024

Claudine Hood has seen a lot of patients dealing with complex medical bills. With more than 20 years as a medical billing professional, she knows that people often find it difficult to understand their medical bills.

Her advice? Be proactive when it comes to handling medical expenses, especially when they are unexpected.

“It’s a good idea to become familiar with how medical billing works for each of your doctors and other medical providers, especially when testing or procedure is involved,” Hood said.

When a medical procedure is planned, you may have time to prepare for any expenses such as insurance copays that may be involved. But emergencies or other unplanned medical events may also result in unexpected expenses.

Unplanned medical emergencies can be overwhelming for patients and their families. Nearly one-fourth of adults in the U.S. faced unexpected major medical expenses during 2022.1

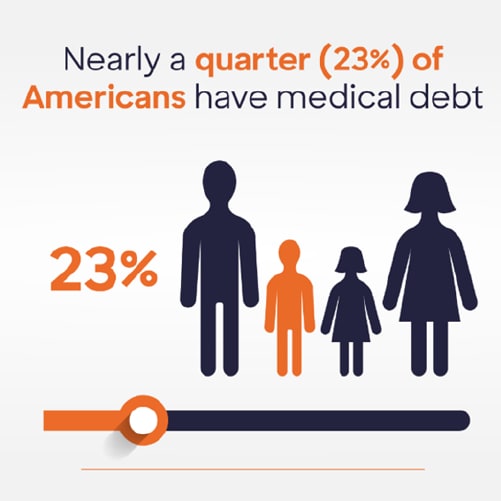

But paying for medical expenses can be stressful even when care is planned. A recent consumer survey by Discover® Personal Loans showed that 61% of Americans say paying for medical care causes them anxiety. And nearly a quarter (23%) of Americans have medical debt and, among them, 16% owe more than $6,000.*

While medical bills on their own do not affect your credit score , they may have an impact if they remain unpaid, are sent to a collection agency, and are reported to a credit reporting agency. That is why Hood recommends that patients and families always work to understand what they are asked to pay.

Repaying unexpected medical expenses can be a burden, and it can be easy to fall behind if you need to make payments to multiple providers. Even bills for planned care may be difficult to place into your family budget.

The good news is that there are several ways to deal with medical debt that can help you limit the impact to your credit.

Unexpected medical expenses may become overwhelming, especially if you are also dealing with a complex diagnosis or procedure. “If someone is having surgery or another procedure, medical bills are often split up in many different ways and in multiple bills,” Hood said.

One medical procedure may involve several medical bills coming from different providers. For example, there may be separate bills for the doctor, the medical facility, and for other providers such as labs and testing, Hood explained. In addition, there may be separate payments due for each provider.

As bills start to add up, you might look to a credit card to pay your medical expenses. This use of revolving credit may impact your credit utilization, which measures the amount of revolving debt you have compared with the total credit you have available. So, if you add debt to your credit card, it may lower your credit score.

“It’s a good idea to become familiar with how medical billing works for each of your doctors and other medical providers, especially when testing or procedure is involved.”

— Claudine Hood

If you don’t pay your medical bills on time, they may be sent to a debt collector. Recent changes in the way medical debts are reported, though, make it possible that some unpaid medical debts will not show up on your credit report, even if they are in collections.

The three nationwide credit reporting agencies recently began removing paid medical debt from credit reports. Further, they have said that medical debt under $500 will no longer appear on credit reports.2 In addition, they will no longer report unpaid medical debt unless it has been in collections for 12 months (up from six months previously).2

To find out if medical debt appears on your credit report, you can contact the three major credit reporting agencies, Experian, TransUnion, and Equifax. You can request a free copy of your credit report each year from each of them.

Review each copy of your credit report to check if there are medical bills listed. They might be listed in the collection-items section of the report. Or they might be listed under the name of the medical provider or medical facility, or by the name of a collection agency.

If you find medical debt on your credit report that should not be there, contact the credit reporting agency to dispute the item. You can also contact the Consumer Finance Protection Bureau or state credit agencies for help submitting a complaint.

Sometimes charges listed on medical invoices or statements may be confusing. There might be charges that you don’t recognize.

To start, Hood advises speaking with the medical billing staff in your provider’s office. “The person who specializes in billing and insurance matters may be able to help you review and understand charges that may be involved, even before a procedure,” she said.

You might also check to make sure that the items on your medical bill or statements are accurate. Sometimes medical bills contain mistakes because someone has added an incorrect diagnosis or procedure code or because of other data-entry errors. Contact your provider if you believe there may be an error on your medical bill.

You should also review your health insurance policy and coverage prior to a procedure, Hood said. “Your doctor’s office may have an insurance specialist whose role is to review and help verify what amounts your health insurance is expected to cover,” she said.

No matter how large or small your medical costs are, knowing how to manage the debt is important. There are several different approaches to deal with incoming bills:

If you have health insurance, it might help you pay some bigger medical expenses and protect your financial health.

Health insurance may cover emergency medical services and potentially prevent future medical expenses by paying for preventive care. It’s important to find out which medical expenses are paid by your health insurance and what deductibles, copays, or other payments you may have to make. In most cases, you likely have a co-pay or coinsurance and possibly a deductible. This means that your insurance may pay a larger portion, but you may owe your practitioners something as well.

In addition, a health savings account (HSA) may help by providing a tax-advantaged option to help pay for medical expenses. Consider consulting with a tax advisor if your medical bills are substantial.

There are various resources for health insurance, including your employer and through government programs, you may contact to find out more.

For costs not covered by insurance, it helps to know your options. Your medical provider may be able to set up payment plans directly through their office. It is important to work with the provider to let them know how much you can afford to pay each month. “I tell patients even sending a small amount every month shows that you are trying to pay the bill in good faith,” Hood said.

Keep in mind that if you have a payment plan with a medical provider and do not pay as agreed, that medical provider may send the balance to collections. Some providers may wait 180 days before sending overdue bills to collections, but others may send a notice sooner.

People often use credit cards to pay for unexpected expenses. If you choose to use your credit card to fund an unexpected medical expense or pay coinsurance, do your best to ensure you can manage the monthly bills so you can minimize the amount of higher-interest you might pay.

The responsible use of credit cards has several benefits, such as flexible payment options and promotional interest rates in some cases. But you don’t want to overextend yourself, as credit cards may carry high interest rates. They can also charge fees if you don’t pay your monthly balance in full.

Depending on your personal financial situation, you may save money in interest over time by using a personal installment loan, because a personal loan may have a lower rate of interest compared to a credit card. In addition, a personal loan may be a better tool for long-term financial planning, as personal loans have a fixed rate and a fixed repayment term. As a result, using one to pay for medical expenses may help you with budgeting for existing or planned medical debt.

Facing medical expenses may be challenging, especially when they are unexpected. But there are solutions and tools that may help you more quickly and easily make a plan to pay for them. Estimate your payments and see if a personal loan works for your situation.

Articles may contain information from third parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third party or information.

*ABOUT SURVEY

A national survey of 1,000 U.S. residents ages 18 and up was commissioned by Discover and conducted by Dynata (formerly Research Now/SSI), an independent research firm, between June 28 and July 3, 2023. The maximum margin of sampling error was +/-3 percentage points with a 90 percent level of confidence.