You may more easily manage major purchases, like last-minute airline tickets or new appliances, when you break them down into multiple monthly payments with your credit card. But credit card debt might cost you in the long run, as credit card issuers typically charge interest on any balance you carry from month to month. If you’re not careful, interest charges may pile up quickly and drastically increase the amount you owe. However, with the right strategies, you may manage interest effectively and avoid excess credit card debt.

How to Avoid Interest on a Credit Card

7 min read

Last Updated: November 6, 2025

Table of contents

Key Takeaways

-

You may avoid credit card interest by paying your statement balance in full by the due date every month.

-

If you can’t repay your entire balance, consider paying more than the monthly minimum to reduce your interest charges.

-

Transferring your balance from a high-interest credit card to a lower-interest card may make your debt more manageable.

How does credit card interest work?

Interest is the cost of borrowing money. If you don’t pay off your full credit card balance by the due date, your credit card company typically applies an interest charge to the remaining balance. Your credit card’s annual percentage rate (APR) determines your interest charges.

While APR is an annual rate, credit card interest accrues daily. To find your daily interest rate, divide your APR by 365 (for the days in the year). Credit card companies charge interest by multiplying your balance by the daily interest rate every day and adding that amount to your debt. While interest fees may seem small initially, they might not take long to pile up.

Ways to avoid or limit credit card interest

Fortunately, practicing responsible credit habits and managing your debt strategically may help you save money on interest. Consider your current circumstances to determine the best next step for minimizing your interest.

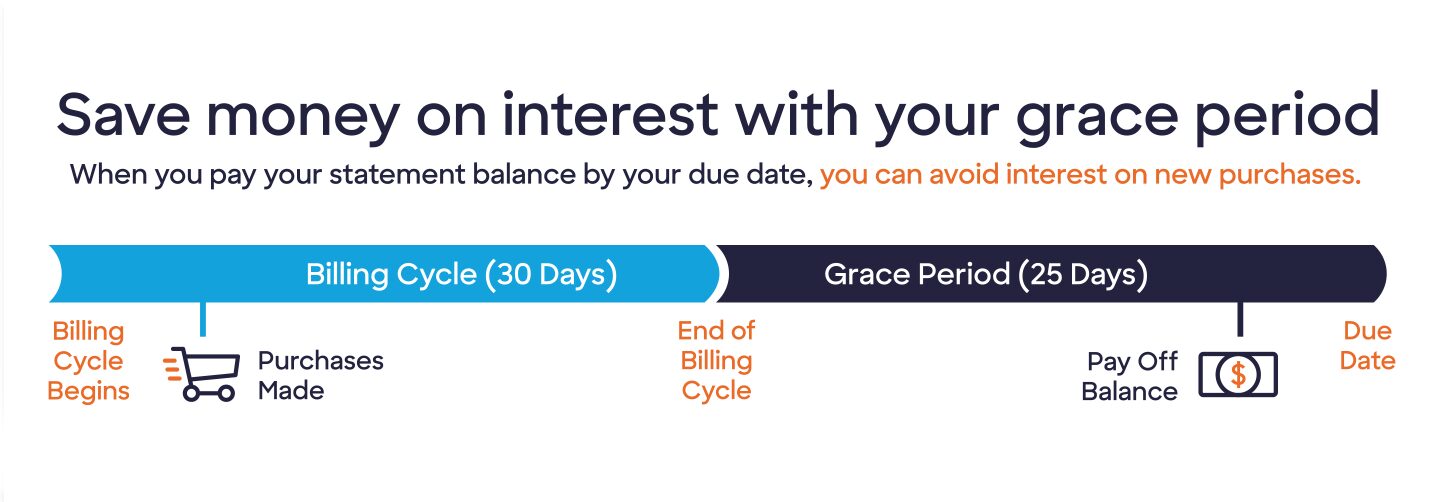

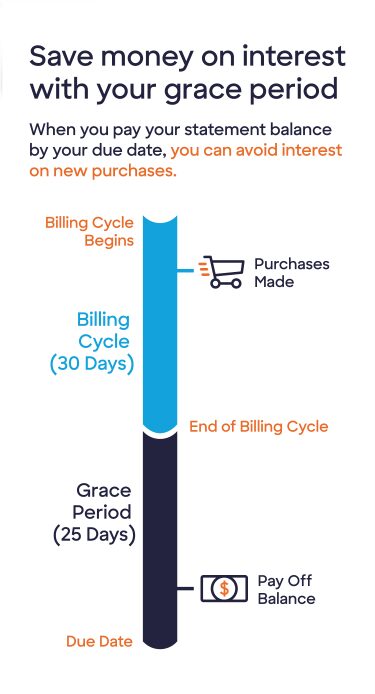

Leverage your grace period

You may avoid interest charges altogether by taking advantage of your credit card’s grace period. According to the Consumer Financial Protection Bureau, a grace period is the time between the end of your billing cycle and your payment due date.

If you pay your statement balance in full by the due date, your purchases during the grace period won’t accrue interest. But if you only make the minimum payment or otherwise pay less than the statement balance, you typically lose the grace period for that billing period and the next. Your credit card issuer will add interest to your purchases at the standard rate.

Credit card issuers aren’t obligated to offer a grace period. But, under the Credit CARD Act of 2009, companies must make sure you receive your credit card bill at least 21 days before the payment due date. So, when card issuers offer grace periods, they must last at least 21 days. Information about a card’s grace period may be available in your credit card agreement. Most credit cards don’t provide a grace period on cash advances or balance transfers.

Put simply, if you pay your credit card balance in full each month, you may not have to pay interest charges on purchases.

Make more than the minimum monthly payment

While repaying your entire monthly balance might save you the most money, it’s not always possible. However, that doesn’t mean unwieldy interest charges are inevitable.

Even if you can’t afford to pay your balance in full, making more than the minimum payment may reduce interest by reducing the time it takes to pay off your debt. Interest charges offset rewards, so shrinking your interest might help you earn more.

Our credit card interest calculator may help you estimate how much you’d save on interest by increasing your monthly payment.

Make multiple credit card payments per month

While you must make at least the minimum monthly payment by your credit card due date to keep your account in good standing, credit card issuers generally let you make payments at any time during the billing cycle.

Since interest grows daily, bringing down your balance throughout the month reduces the overall amount of interest you pay.

Making multiple monthly payments might make sense in several situations. For example, if you’re paid on a bi-weekly basis, you might put a portion of both checks toward your credit card balance. Or, if you shop with your cash back credit card to earn rewards, consider paying off new purchases right away instead of letting them accrue interest.

Get a credit card with a balance transfer offer

If you’re struggling to pay off the balances on one or more credit cards with high interest rates, a balance transfer to a credit card with a low introductory interest rate may help you get your debt under control. Many credit card issuers offer balance transfer promotions with a 0% or low APR for a set period after account opening.

During the introductory period, you may pay down your credit card balance without high interest charges. But any balance that remains on the account after the introductory period ends typically begins accruing interest at the standard rate. So, it’s crucial to have a plan for repaying your balance.

Most credit card issuers charge a balance transfer fee, which may be a flat fee or a percentage of the balance you move. Before applying for a balance transfer credit card offer, make sure your savings outweigh the costs.

Enroll in autopay

You may enroll in autopay to manage your credit card bill and keep your balance low. Autopay allows your credit card issuer to withdraw funds from a bank account of your choosing automatically and apply them to your credit card account before your payment due date. By setting your autopay to an amount that’s greater than your minimum monthly payment, you may gradually pay down your outstanding balance and lower your interest charges. Plus, you may avoid hurting your credit score or owing a late fee due to a missed payment.

Limit cash advances

The types of credit card transactions you make may also influence your interest charges. Credit card companies often charge a higher interest rate for cash advances than for regular credit card purchases.

Cash advances allow you to borrow cash against your credit limit, usually by withdrawing funds from an ATM. Interest typically begins building as soon as you take out a cash advance. Plus, your card issuer may charge cash advance fees on top of ATM fees.

Alternatives to a cash advance, like a personal loan, may help you access money quickly at a lower interest rate.

Consider buy now, pay later for large purchases

A buy now, pay later (BNPL) plan is an alternative to credit cards that allows you to break purchases down into monthly installments, sometimes without interest.

BNPL plans are often convenient, and they might save you money in some cases. However, terms, rates, and conditions may vary a lot from provider to provider. Make sure you understand potential costs, like the service’s late fee amount, before you apply.

How do credit scores affect your interest rate?

Factors like your credit report, credit score, and financial background influence the APR offers you qualify for. You may need an excellent credit score to qualify for the best credit card interest rate available to you. The following responsible credit habits may help you build positive credit history:

- Pay your credit card bill on time each month.

- Keep your credit utilization (the percentage of your available credit in use) low.

- Avoid applying for multiple credit cards within a short time period.

- If you only have a credit card account, consider other types of credit, like personal loans, to improve your credit mix. But only apply for as much credit as you need.

The bottom line

A credit card may help you tackle expensive purchases, even if you don’t have all the cash in hand. But before you shop, make sure you have a plan for paying down your balance and managing interest charges. That way, you may enjoy the convenience a credit card offers without the stress of mounting credit card debt.

See if you’re Pre-approved before you apply

Next steps

See if you're pre-approved

Learn about Discover It® Cash Back Credit Card

See rates, rewards and other info

You may also be interested in

Was this article helpful?

Was this article helpful?