What is a hardship withdrawal for 401(k)? Here’s what you need to know

If you’re thinking of withdrawing money from your 401(k), it’s important to understand if you’re eligible, how the process works, and what the potential downsides are before tapping into retirement savings.*

In a perfect world, your finances and goals are completely mapped out, and your journey from milestone to milestone is a smooth ride. But no matter how much you plan, life’s unexpected hardships are just that: unexpected. A financial speed bump can be a jolt to the system, but it doesn’t have to bring you to a stop.

When you need cash, one of your first instincts may be to tap into savings. If you have an emergency fund saved up, that should be your first choice. But if you don’t and are thinking about drawing from your retirement savings, you’re probably wondering: What is a 401(k) hardship withdrawal and should I take one?

With help from Arielle O’Shea, investing and retirement specialist, and Sam Dogen, founder of a personal finance website, here’s what you need to know about a 401(k) hardship withdrawal and how it may affect your retirement planning:

401(k) hardship withdrawal: What it is and how to know if you’re eligible

A 401(k) hardship withdrawal is an early distribution from a 401(k) account to pay for an “immediate and heavy financial need,” as defined by the IRS.

While it’s typically difficult to pull out funds from your 401(k) before age 59½, some employers and plan providers allow hardship withdrawals for plan participants with qualifying financial needs. But, if you decide to withdraw early you’ll likely face penalties, which can be steep. (After age 59½, the IRS allows penalty-free withdrawals based on your 401(k) plan’s terms.)

If you’re considering a 401(k) hardship withdrawal, here’s what you need to research:

Understand what qualifies

The IRS offers guidance around what constitutes a qualifying financial need. Each 401(k) plan will define its own qualifications and determine if you’re eligible for a 401(k) hardship withdrawal given your particular situation, O’Shea says. As you’re learning 401(k) hardship withdrawal rules, note that common qualifying financial needs include:

- Costs directly related to the purchase of a home (excluding mortgage payments)

- Payments to avoid home foreclosure or eviction

- Funds to cover significant damage to your home caused by a natural disaster

- College tuition, fees, or room and board for you, your spouse, or dependents

- Medical bills

- Funeral and burial expenses

Learn about withdrawal limits

When determining how much to withdraw from your 401(k), it’s important to know that your withdrawal is limited to the amount you need to cover the expense, according to the IRS.

While there isn’t technically a limit on the number of 401(k) hardship withdrawals you’re allowed in a year, you are limited by whether you qualify and whether you have enough money in your 401(k) to cover the qualifying hardship amount. You’ll also have to work with your plan sponsor and/or HR department to prove your hardship and provide proper documentation, per the plan’s 401(k) hardship withdrawal rules.

Look into eligibility requirements

Another key consideration is whether you’re eligible for a 401(k) hardship withdrawal. Keep in mind that not all 401(k) plans and employers allow hardship withdrawals, and, among the plans that do, qualifications and 401(k) hardship withdrawal rules may vary from those listed by the IRS.

“Here’s the tricky thing: Each plan sets the rules around this separately,” O’Shea says. “Your 401(k) plan documentation is the best source to find out what qualifies for a hardship under your plan’s rules.”

Stay up to date on legislative changes

Lastly, if you’re considering taking one, realize that 401(k) hardship withdrawal rules can change. For example, the Coronavirus Aid, Relief and Economic Security (CARES) Act made it easier for those affected by COVID-19 to take hardship withdrawals without penalties in 2020.

“Your 401(k) plan documentation is the best source to find out what qualifies for a hardship under your plan’s rules.”

Be sure to do your research to understand if a law or policy change will make it more or less advantageous to take a withdrawal.

After researching 401(k) hardship withdrawal rules and whether you’re eligible for a hardship withdrawal, your next step should be assessing the potential impact on your finances.

The downsides of taking a 401(k) hardship withdrawal

Even if a 401(k) hardship withdrawal is available to you, it’s not something you want to do on a regular basis, if at all, says O’Shea. Given the penalties and taxes, “Taking a hardship withdrawal is generally a last resort,” she says.

In addition, Dogen notes, you’ll be depleting your retirement savings—a decision that can have long-term ramifications.

If you are thinking about a 401(k) hardship withdrawal, be sure to consider how taking money out now may affect your future. Here are some of the factors you should consider as you decide whether it’s right for you:

You’ll likely pay penalties and taxes

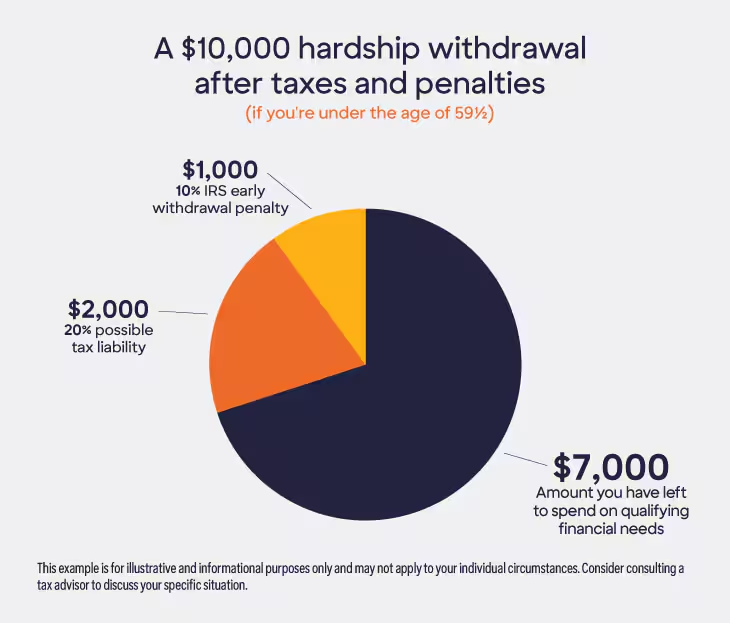

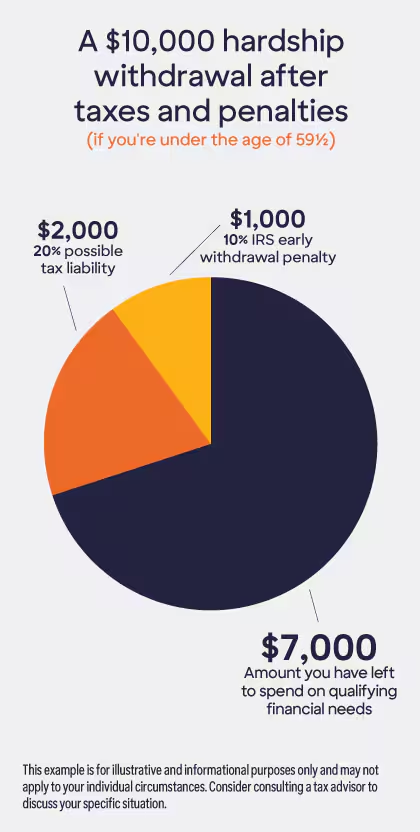

It’s important to note that you’ll typically have to pay an early withdrawal penalty of 10% plus taxes if you make a 401(k) hardship withdrawal.

“Because of the penalties and taxes you’ll incur, you should only consider a hardship withdrawal if other options aren’t available to you and you genuinely need this money,” O’Shea notes.

On the tax side, hardship withdrawals may be subject to tax withholdings.

It can take time to rebuild your savings

Another potential downside is the fact that you can only contribute a limited amount of money to your 401(k) each year due to IRS limits. You can’t immediately put all the money back into your account, according to the IRS.

“If you pull a big chunk of money out, even if you have the money to max it out every year, you’ll have to replenish the funds very slowly over time,” O’Shea says.

For example, in the 2025 tax year, you can contribute a max of $23,500 to your 401(k) account, the IRS says. If you’re 50 and older, you can also take advantage of catch-up contributions—up to an additional $7,500 per year.

That means, if you’ve taken $60,000 out of your 401(k) account to cover a hardship, it may take two years to put that amount into your account if you’re over 50 and maxing out your contributions, and almost three years if you’re under 50.

You’ll miss out on potential ROI

When you take funds out of your 401(k), you’re also taking them out of the market. Imagine you receive a 5-8% average annual return on your 401(k) each year. When you pull a chunk of money out of that account, those funds can no longer compound and earn a return. This may be the biggest downside to taking a hardship withdrawal, Dogen says.

O’Shea also says that, depending on how the market is performing, you may end up selling your investments at a loss. “You have to sell the investments in your account in order to cash that money out, and so if the investments are down when you sell, you’re locking in that loss,” O’Shea says.

3 alternatives to 401(k) hardship withdrawals

Given 401(k) hardship withdrawal rules and the financial ramifications of a 401(k) hardship withdrawal, it’s crucial to fully vet any other ways you could obtain the funds to cover the hardship. “You would want to exhaust all other options first,” O’Shea says.

Consider these alternative sources of liquid funds:

Withdraw funds from your savings account

When you’re in need of money for unexpected expenses, first consider pulling funds from an emergency fund or a savings account, O’Shea says.

If that’s not available to you, she recommends you see whether you’re able to withdraw funds from a certificate of deposit or money market account. If you do pursue those types of withdrawals, look into what fees and penalties you would incur before you pull out your money.

Tap into your other retirement accounts

If you have a Roth IRA, you might want to explore a contribution withdrawal from that account as an alternative to a 401(k) hardship withdrawal, O’Shea notes. That’s because you can withdraw contributions you’ve made into a Roth IRA at any time without paying taxes or IRS penalties, O’Shea explains. The reason? You’ve already paid taxes on those contributions.

Borrow from your 401(k) with a 401(k) loan

If your 401(k) is the only funding you can access to cover your hardship, you may consider borrowing from your 401(k) with a 401(k) loan, O’Shea says.

How much you can borrow from your 401(k) depends on your plan. Account holders can typically borrow up to 50% of their 401(k) account balance or $50,000—whichever is less, O’Shea says. You can take out a 401(k) loan before age 59½ with no penalty, Dogen explains.

Unlike a 401(k) hardship withdrawal, a 401(k) loan requires you to repay the funds you’ve borrowed back into your account. That’s actually a benefit, because your money goes back into your 401(k) once you repay the loan. In most cases, you’ll have five years to repay a 401(k) loan.

Still, keep in mind, borrowing from your 401(k) is not a risk-free option. If you can’t pay the loan back and you’re under 59½, it may be deemed an early distribution by the IRS, and you could owe taxes and a 10% early withdrawal penalty, O’Shea says. Consider consulting a tax advisor to discuss your specific situation.

“You can ask your HR department for an estimate as far as when you might be able to get the money—it’s going to vary by plan.”

The 401(k) hardship withdrawal process

If you’re considering a 401(k) hardship withdrawal and are still employed, O’Shea recommends speaking with your company’s HR department to understand your specific 401(k) hardship withdrawal rules.

If you’re unemployed, you’ll need to speak to your plan provider to determine if you can take a 401(k) hardship withdrawal, O’Shea says. From there, it’s a matter of filling out paperwork to submit your request, O’Shea says.

Note that there’s always a chance your request will be denied. Some employers may require you to prove that you’ve exhausted all other options for funding. If your employer doesn’t deem your hardship as immediate or necessary, your request can also be turned down, O’Shea says.

The entire process may take a few weeks, she adds. “You can ask your HR department for an estimate as far as when you might be able to get the money—it’s going to vary by plan.”

Rebuilding your savings after a 401(k) hardship withdrawal

After taking a 401(k) hardship withdrawal, it may take a while to regain your financial footing. That’s to be expected. But once you’re back on your feet after your hardship, O’Shea recommends you ramp up savings efforts as quickly as possible. That will help you sidestep some of the most common retirement savings mistakes.

So you don’t get behind on your retirement savings, make sure you’re contributing enough to your 401(k) to take advantage of an employer match, if possible. Eventually, try to max out your annual 401(k) contributions—including catch-up contributions if you’re over 50, O’Shea says.

“This period is really about trying to recover, focusing on getting yourself financially stable and doing everything you can to catch up,” O’Shea says.

As you look to the future, you’ll want to strengthen your financial situation so you can avoid taking another 401(k) hardship withdrawal. Looking for a good place to start? Learn how to start an emergency fund in four steps.

Give your emergency fund some serious momentum with a great rate that helps every dollar go further.1

1The claims made regarding the competitiveness of our 360 Performance Savings account rate are based on Curinos Inc. national percentile data for savings accounts on balances of $1.

Articles may contain information from third parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third party or information.

* The article and information provided herein are for informational purposes only and are not intended as a substitute for professional advice. Please consult your tax advisor with respect to information contained in this article and how it relates to you. Nothing contained in this article shall give rise to, or be construed to give rise to, any obligation or liability whatsoever on the part of Discover, a division of Capital One, N.A., or its affiliates.