It doesn’t matter how much you earn in credit card rewards if you can’t use those rewards in ways that matter to you. Luckily, with rewards credit cards like the Discover it® Cash Back Credit Card or the Discover it® Miles Credit Card, you can redeem your rewards for cash at any time1. And you can even use any amount of rewards to help pay for your next Amazon.com purchase2.

Use Your Discover® Rewards at Amazon.com

Last Updated: October 16, 2023

2 min read

Key points about: using Discover rewards at Amazon.com

-

Log in to your Discover Card account to link your card with your Amazon.com account and enroll in Shop with Points.

-

After your accounts are linked, you can set your Discover Card as your default payment method at Amazon.com.

-

If you’re eligible and have rewards available on your account, you may be able to “Shop with Points” using the cash back or Miles you’ve earned on your Discover Card.

When you link your Discover Card to your Amazon.com account, you can start paying for your Amazon.com purchases by redeeming your credit card rewards.

Did you know?

Once you link your Discover Card with your Amazon.com account, you can begin redeeming your rewards at Amazon.com checkout. Just add items to your shopping cart and proceed to the regular checkout process. You’ll see rewards available for use next to your Discover Card.

But how does it work? Discover it® Cash Back Card Cashback Bonus® or your Discover it® Miles Card rewards can be redeemed towards your purchase at Amazon.com checkout. You can redeem as much of the rewards you’ve earned as you’d like.

To use your Discover it® Cash Back Card’s Cashback Bonus® or your Discover it® Miles rewards to shop at Amazon.com, you simply link your Cash Back Card or your Miles Card to your Amazon.com account and enroll in Shop with Points following the below steps. Once you do that, you can redeem any amount of your rewards at Amazon.com—there's no minimum.2 It’s one of the great ways a credit card with rewards can bring more value to your shopping.

Ready to get started?

How to pay with rewards at Amazon.com

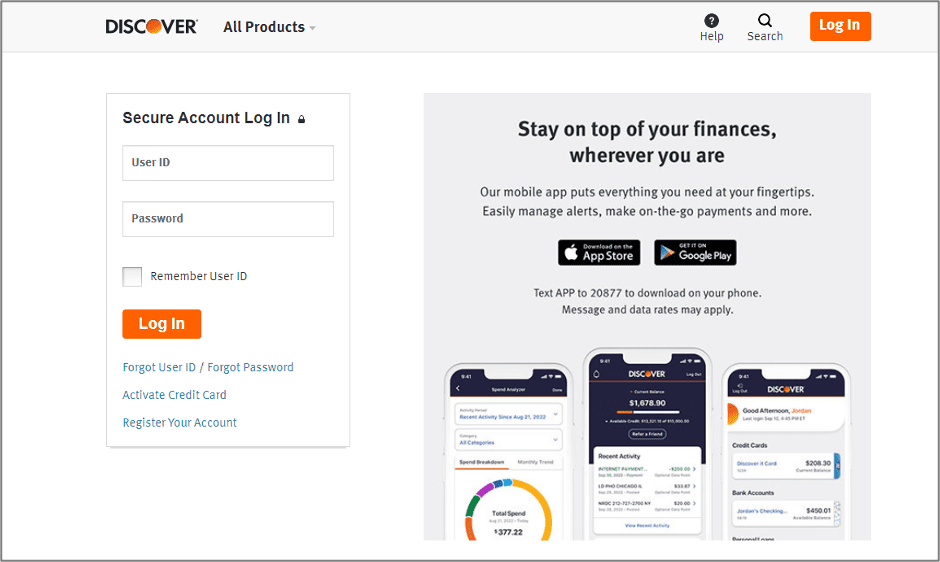

After logging in using the link, you’ll be brought to the below page, prompting you to add your card to your Amazon.com account.

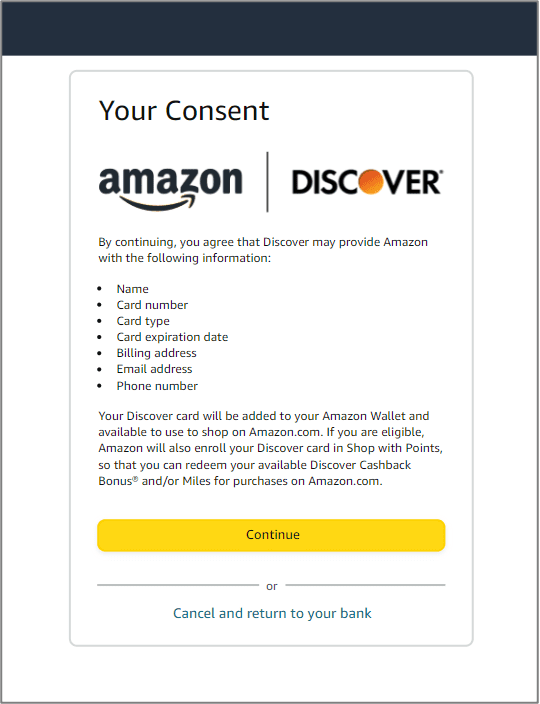

Next, review the terms and conditions and click the “Add Card” button.

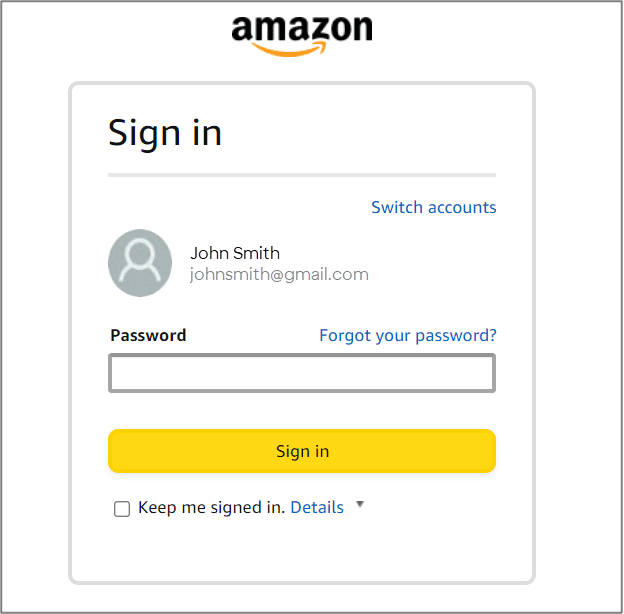

You’ll then be prompted to sign in to your Amazon.com account. After clicking the “Sign in” button, you’ll be taken to the below page.

Review the terms. After clicking “Continue,” you’ll receive confirmation that your card was successfully linked to your Amazon.com account.

Once your Discover Card is linked to your Amazon.com account, you can set your card as the default payment method in your Amazon.com Wallet. From the Wallet page, hover over the card you’d like to set as your default payment method and click “Edit.”

A pop-up box will appear. You can then click the checkbox to select this credit card as your default payment method. Click “Save” to update your default payment method.

Now when you check out, this Amazon.com account will select your Discover Card to pay. (You can change your payment method at checkout as needed.)

Once you link your Discover Card with your Amazon.com account, you can redeem your rewards at Amazon.com checkout. Just add items to your shopping cart and proceed to the regular checkout process. You’ll see rewards available for use next to your Discover Card.

Enter the rewards amount you’d like to redeem for your Amazon.com purchase and click “Apply.” Use any amount of your rewards to help pay for your Amazon.com purchase.

See if you’re Pre-approved before you apply

There’re no impact to your credit

Next steps

See if you're pre-approved

No impact to your credit score

View all Discover credit cards

See rates, rewards and other info

You may also be interested in

Was this article helpful?

Was this article helpful?

- Rewards never expire. We reserve the right to determine the method to disburse your rewards balance. We will credit your Account or send you a check with your rewards balance if your Account is closed or if you have not used it within 18 months.

- Use Rewards at Amazon.com: For complete details on how to Pay with Rewards at Amazon.com see Amazon.com/DiscoverRewards. Amazon is not a sponsor of this promotion. Amazon, the Amazon.com logo, the smile logo and all related marks are trademarks of Amazon.com, Inc. or its affiliates. To redeem your rewards at checkout, you must select the Discover Card from which you want to redeem rewards. If you do not pay for your full purchase with rewards, you may use the Discover Card from which the rewards were applied or an Amazon.com Gift Card to pay for the remainder of your purchase. You may not use a credit card from an issuer other than Discover or another Discover credit card enrolled in Shop with Points in conjunction with the rewards transaction.

-

Legal Disclaimer: This site is for educational purposes and is not a substitute for professional advice. The material on this site is not intended to provide legal, investment, or financial advice and does not indicate the availability of any Discover product or service. It does not guarantee that Discover offers or endorses a product or service. For specific advice about your unique circumstances, you may wish to consult a qualified professional.