ACH vs. wire transfer: What’s the difference?

While automated clearing house payments and wire transfers are both electronic solutions for moving money, they serve different purposes. Understanding their costs, speed, and security features can help you choose the best option.

Electronic money transfer technology has made banking transactions much easier. Whether you’re adding funds to a new account or moving funds between bank accounts or across financial institutions, such transfers can make the process much more seamless. Two of the most common methods are automated clearing house (ACH) transfers and wire transfers.

While both allow you to send money electronically—often from the comfort of your own computer or mobile device—there are some key differences worth understanding in order to fully assess ACH vs. wire transfer technology.

What is an ACH payment?

An ACH payment moves funds electronically between verified customer bank accounts through the automated clearing house network at different financial institutions. Developed in the early 1970s as a more efficient alternative to paper checks, the ACH system has since become one of the primary methods of electronic money movement. A consumer who is an account holder at two different banks can move funds between the two accounts thanks to this technology.

ACH transfers are processed in batches by ACH operators, such as the Federal Reserve and clearinghouses, which are financial companies that facilitate the exchange of funds or other assets between two parties.

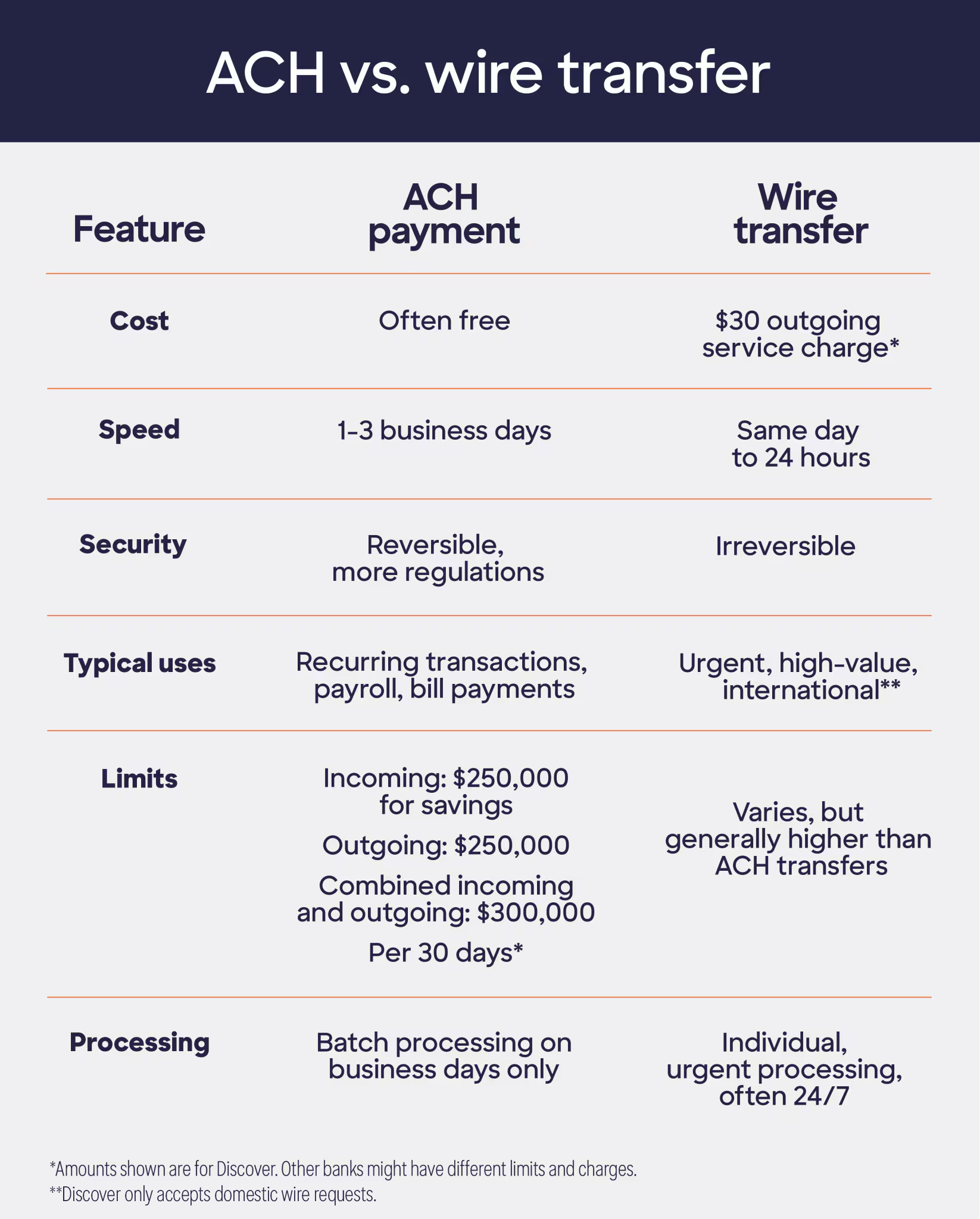

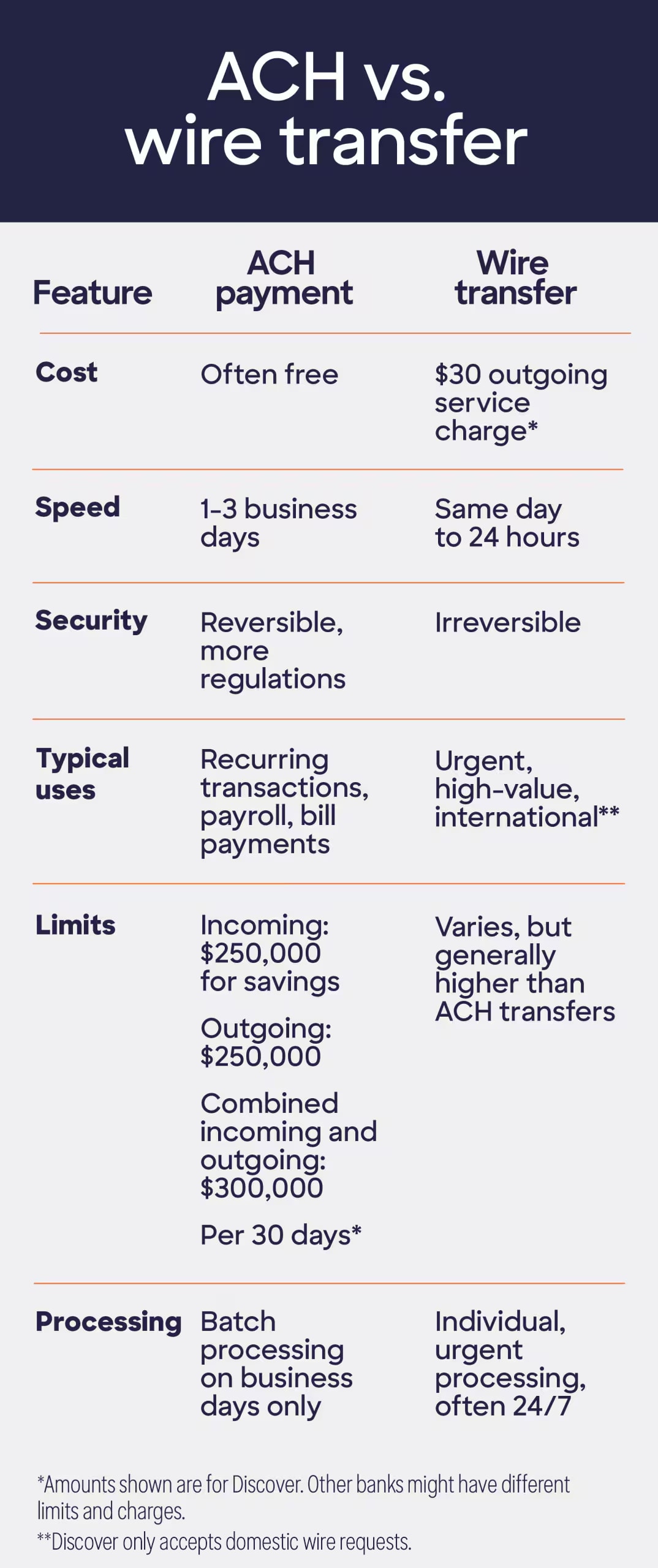

A common question is: How long does an ACH transfer take? Typically, they take one to three business days to complete, as they are processed overnight on business days only. Additionally, ACH transfers often come with little to no cost.

Receiving your paycheck via direct deposit is one common example of an ACH payment. But you can also use ACH transfers to pay recurring bills like utilities, rent, mortgages, subscriptions, and gym memberships. Other ACH options include online purchases and transferring funds between accounts at different banks or financial institutions.

The difference between ACH and wire transfers often comes down to factors like cost and transaction time.

Pros and cons of ACH transfers

Before you process an ACH transfer, consider the advantages and potential downsides.

Pros of ACH transfers:

- Cost savings: Depending on your bank, ACH transfers are often free.

- Recovery option: ACH transfers are reversible in the event of unauthorized or fraudulent transfers.

- Strong security: ACH transfers are considered very secure, with additional regulations and consumer protections in place to prevent theft.

Cons of ACH transfers:

- Wait time: It typically takes one to three business days to complete an ACH transfer, so it’s not the best option if funds are needed immediately.

- Global restrictions: Depending on your bank, you may only be able to use ACH to transfer funds domestically.

- Transfer limits: ACH payments typically have lower transaction limits than wire transfers as well as daily or monthly caps (depending on the bank). These limits can impact how much you regularly add to an online account. For example, incoming ACH limit for a savings account at Discover®—per 30-day rolling period—is $250,000. Outgoing limits are $250,000, and the combined incoming/outgoing limit per 30-day rolling period is $300,000.

What is a wire transfer?

A wire transfer also moves funds electronically between financial institutions, but goes through different networks than ACH, such as SWIFT (for international transfers) or Fedwire (for domestic transfers). Wire transfers can help you expedite payments because they are processed individually and continuously, allowing funds to be available within hours in most cases.

The most common types of wire transfers include high-value purchases like a down payment on a home, urgent transactions that need to be settled quickly, business transactions, and international fund transfers.

Pros and cons of wire transfers

Before you make a wire transfer online, you should weigh the speed of transactions against the cost.

Pros of wire transfers:

- Real-time transactions: In many cases, transferred funds are available on the same day.

- Higher transfer limits: Wire transfers typically have higher limits than ACH transfers, making them a better option for expensive transactions.

- No geographic limits: Unlike ACH transfers, you can send money internationally via wire transfers. But you can only move funds domestically via wire transfer at Discover.

Cons of wire transfers:

- Less secure: Compared to AHC transfers, you could encounter more security risks with wire payments, as scammers commonly use them.

- More expensive: Expect to pay $25 to $50 for outgoing transfers. Incoming wire transfers are often less expensive—or even free. (At Discover, there is a $30 service charge for each outgoing wire transfer sent from your account.)

- No recovery option: Funds sent via wire transfer can’t be reversed once sent, even if you’re a victim of fraud.

Deciding between ACH vs. wire transfers

The difference between ACH and wire transfers often comes down to factors like cost, transaction time, and security considerations. ACH transfers are cheaper, more secure, and best for everyday transactions, but can be slower to complete and limited to domestic fund transfers. Wire transfers are faster, allow for global transactions, and can handle larger amounts—but they’re also more expensive, irreversible, and potentially riskier.

Before you make an electronic money transfer, you’ll need to assess your specific needs to determine which method to choose.

Articles may contain information from third parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third party or information.

The information provided herein is for informational purposes only and is not intended to be construed as professional advice. Nothing contained in this article shall give rise to, or be construed to give rise to, any obligation or liability whatsoever on the part of Discover, a division of Capital One, N.A., or its affiliates.